Beta Coefficient: A Measure of Systematic Risk and Applications in Portfolio Management

In the fields of finance and investment, risk and return are two sides of the same coin. To measure this relationship scientifically, economists developed the Beta coefficient (). This research paper provides a detailed analysis of the Beta coefficient, from its mathematical nature to its practical implications for individual investors."

1. What is the Beta Coefficient?

The Beta coefficient () is an index that measures the volatility or systematic risk of an asset (typically a stock) or an investment portfolio relative to the overall market.

In financial analysis, the overall market (represented by indices such as the VN-Index in Vietnam or the S&P 500 in the US) is considered to have a Beta of 1.0. The Beta coefficient indicates how a stock's price responds to market fluctuations:

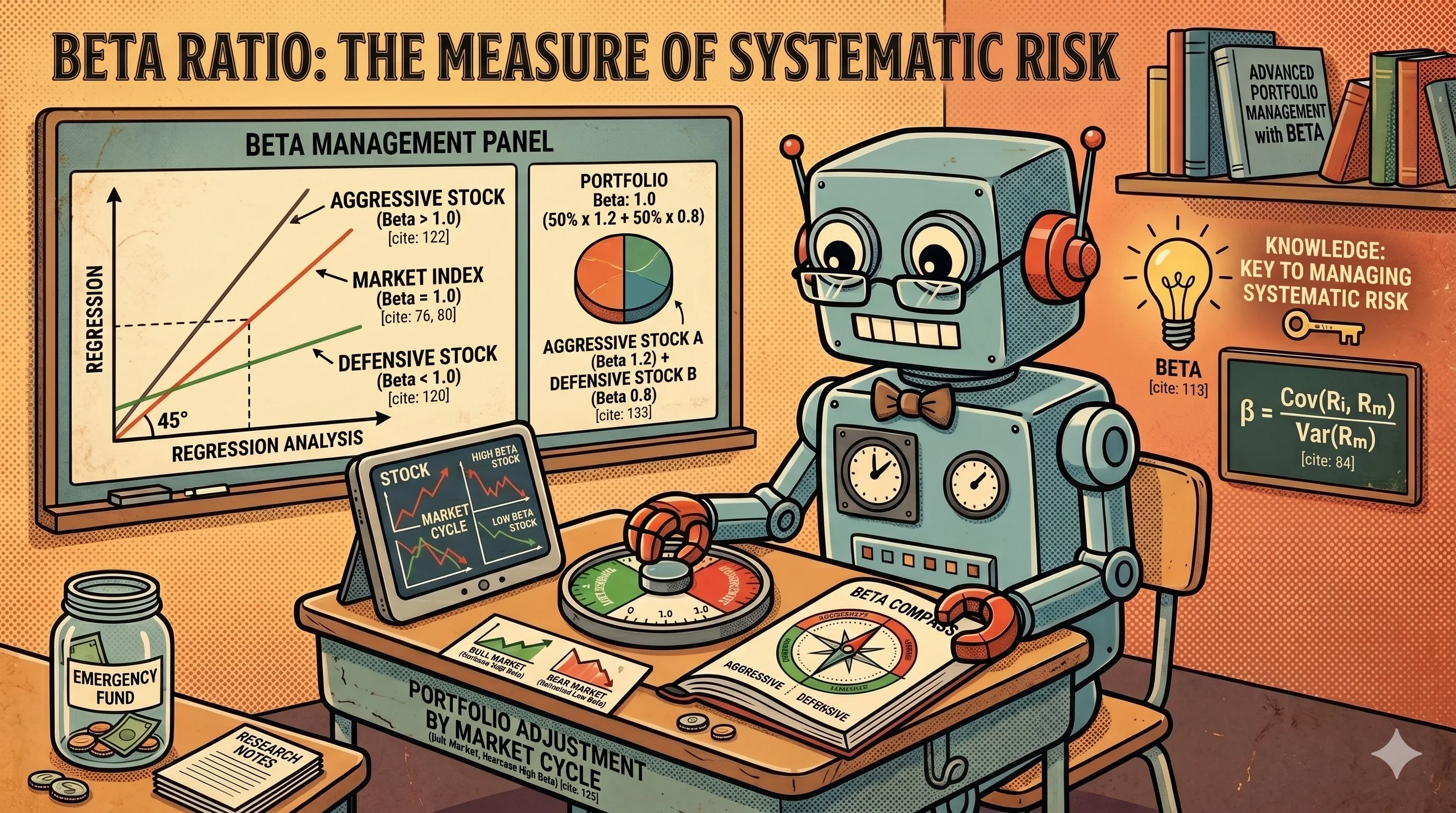

- : The stock tends to be more volatile than the market.

- : The stock tends to be less volatile than the market.

- : The stock moves in tandem with the market.

2. Calculating the Beta Coefficient

The Beta coefficient is calculated using the linear regression statistical method. It is the slope of the line describing the relationship between the stock's rate of return and the market's rate of return.

Mathematical Formula:

Where:

- : The rate of return of stock over a specific period.

- : The rate of return of the overall market.

- : The covariance between the stock's return and the market's return.

- : The variance of the market's return.

In practice, investors typically use historical data from the last 3 to 5 years (weekly or monthly) to calculate this figure.

3. The Role of the Beta Coefficient in Investing

The Beta coefficient acts as a "compass" helping investors navigate a volatile market environment:

- Determining Expected Return (CAPM Model): Beta is a core component of the Capital Asset Pricing Model. It helps determine the return an investor should require based on the risk they accept.

- Asset Classification: It helps investors distinguish between "aggressive stocks" (High Beta) and "defensive stocks" (Low Beta).

- Portfolio Construction: It allows investors to adjust the "sensitivity" of their entire portfolio as desired by combining assets with different Betas.

4. What Happens if We Ignore the Beta Coefficient?

Ignoring the Beta coefficient is similar to driving a car without paying attention to speed or road conditions. Potential consequences include:

- Psychological Shock during Market Corrections: If you own a portfolio of stocks with without knowing it, when the market drops , your assets will evaporate by . This often leads to panic-selling and poor decision-making.

- Mismatch with Investment Goals: An investor prioritizing safety who inadvertently chooses high-Beta stocks will see their long-term financial plan threatened by excessive volatility.

- Failure to Capitalize on Market Cycles: Ignoring Beta means missing out on opportunities for breakout returns when the market enters a strong uptrend.

5. The Relationship between Beta and Risk

In investing, risk is divided into two main types:

- Unsystematic Risk: Risks specific to a business (e.g., a factory fire, personnel changes). This type of risk can be eliminated through portfolio diversification.

- Systematic Risk: Risks that impact the entire economy (e.g., inflation, war, monetary policy). This risk cannot be eliminated through diversification.

The Beta coefficient is the measure of Systematic Risk. A stock with a high Beta does not necessarily mean the company is performing poorly; rather, it means the stock price is extremely sensitive to macroeconomic factors. Therefore, Beta helps investors understand the portion of risk they "cannot escape" when participating in the stock market.

6. Applying the Beta Coefficient for Individual Investors

Individual investors can use Beta to optimize their strategies through the following steps:

a. Stock Selection Based on Risk Appetite

- Conservative Investors: Focus on stocks with . These are usually found in utility, food, and pharmaceutical sectors.

- Aggressive Investors: Look for stocks with . These are typically in the securities, real estate, and technology sectors.

b. Portfolio Adjustment According to Market Cycles

- Bull Market: Increase the weight of High Beta stocks to "ride" the growth wave, helping returns outperform the general index.

- Bear Market/Sideways: Shift toward Low Beta stocks or cash to protect gains and minimize asset drawdown.

c. Calculating Beta for the Entire Portfolio

Investors can calculate the average Beta of their portfolio by taking the sum of each stock's Beta multiplied by its corresponding weight.

Example: If you allocate of your capital to Stock A () and to Stock B (), the portfolio Beta will be:

7. Conclusion

The Beta coefficient is not a tool for precise price prediction, but it is an excellent risk management tool. Understanding and effectively applying Beta allows individual investors to stop being passive in the face of market waves, thereby building a sustainable investment roadmap that aligns with their personal psychology.